21.60%

21.60%

Nasdaq Composite

15.20%

15.20%

S&P 500

13.38%

Dow Jones Industrial Average

0.67%

In June Bloomberg Aggregate Bond Index

2.47%

In June Bloomberg U.S Corporate High Yield Index

Geopolitical and Economic Update:

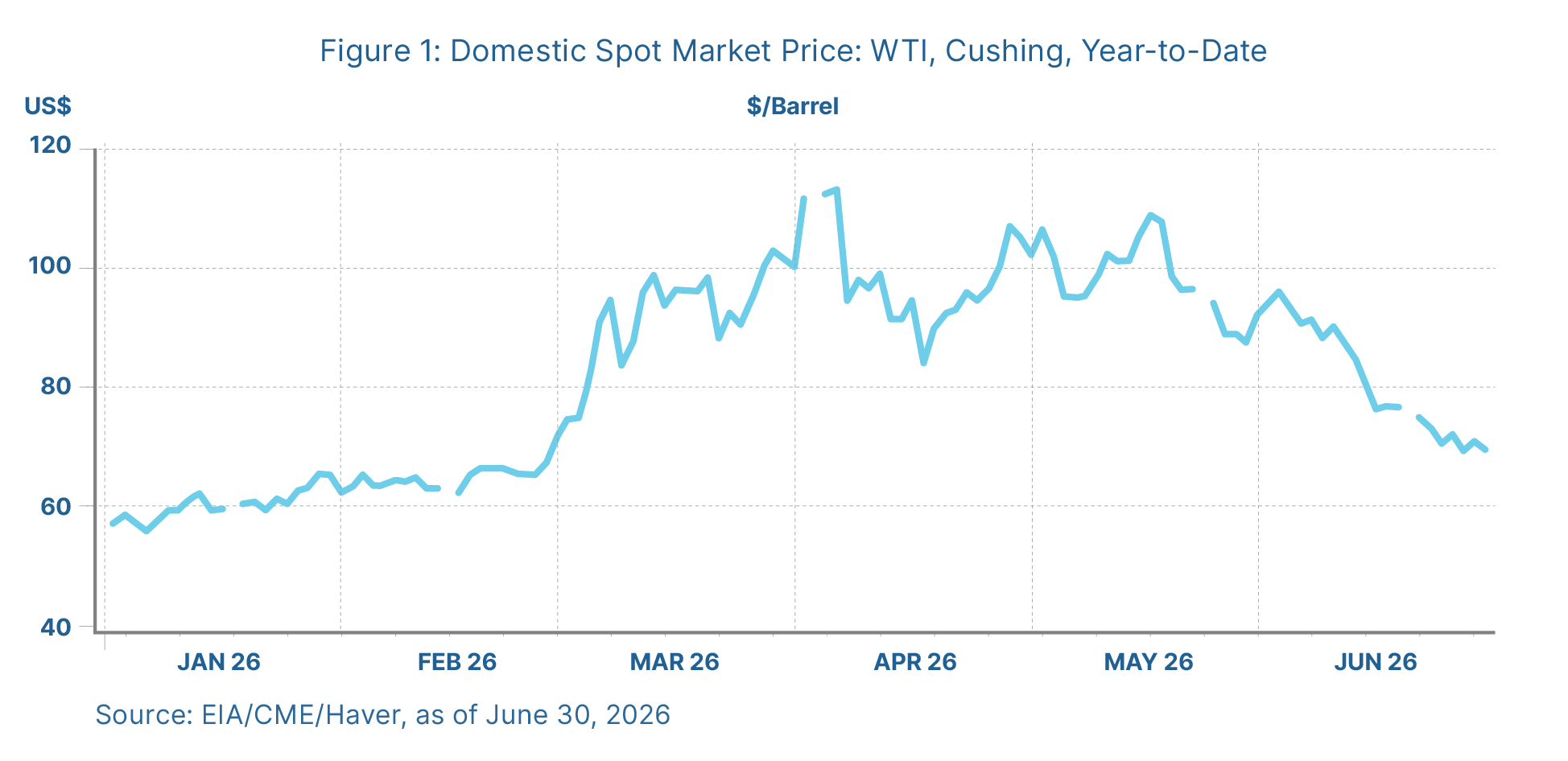

Reopening the Strait of Hormuz Becomes the Key

Economic data over the quarter continued to be supportive of solid economic growth. The employment picture continued to improve after a challenging first quarter for job seekers. Despite consumer confidence indicating concerns persist about the future, retail sales showed consumers are still willing to spend.

The fly in the ointment remains inflation, which has moved higher due largely to increased oil prices flowing through the system. The most recent readings showed consumer price inflation and producer price inflation exceeded 4 percent and 6 percent annually, respectively.

Despite fits and starts in negotiations since the signing of the MOU, the market appears to have discounted a full reopening of the Strait of Hormuz. Oil prices closed out June at levels not seen since the war started in February.

While traffic through the Strait has increased recently, it remains well below the levels seen in February. If negotiations ultimately lead to a full reopening and return of oil supply to global markets, this would be a positive sign for inflation through the remainder of the year.